It’s boggling to see where we were at the beginning of the year and thinking about financial goals and challenges. Three months later we had to adjust our thinking as the coronavirus pandemic spread across the world.

Many of us were suddenly out of work.

We might have been making a little headway on busting our debt and saving money. Starting the journey to become financially better.

Kaboom!

Coulda Woulda Shoulda

Things are not looking good financially. Less income – or no money coming in at all – and we’re struggling to figure out how to pay for our basic necessities. And then don’t we hate it when we start reading a plethora of articles basically saying the same thing.

You should have had an emergency fund.

Yeah OK. We get it.

You with your high paying job – that you still have – and your mortgage free home, and all your investments, and no credit card debt.

Thanks. We get it.

You’re the wonderful saver, investor, planner, budgeter and the rest of us suck when it comes to money matters.

Anyway, I already covered what I think about that topic. Click the banner below for that refresher!

Sad stories

There are a lot of unfortunate stories about people whose lives have been affected by Covid-19. Illness and death and suffering.

And all we’re bitching about is the financial hit we’re taking. We’re struggling to survive. No income. No emergency savings. Not enough money in the bank account to cover the next rent or mortgage payment. No money to buy food. Credit cards are maxed out.

The people who are really struggling to survive are in the hospital’s ECU hooked up to a ventilator.

Right now there is somebody worse off than you, I guarantee it.

My baby steps financial plan

I had to adjust my financial plan as I’m sure many others have also had to do. That is if we even had any sort of financial plan.

Here’s what my Covid-19 adjusted financial plan looks like:

- Incur no debt

- Don’t look at the current value of my investments

- Don’t sell any stocks

- No unnecessary spending

- Build up my emergency fund

- Try to save a little for next year’s TFSA

When it comes to number 6, my goal has been to put $500/month into my savings account for next year’s TFSA – a Canadian financial product called the Tax Free Savings Account. We can deposit $6,000/year. This amount carries over. If you didn’t put in the full amount or didn’t contribute at all for a few years you can catch up to the tune of $69,500 total contributions, assuming you were at least 18 years old in 2009 when the TFSA program began.

If we have no income, saving for retirement has to take a back burner. I was unable to contribute any money to my TFSA dedicated savings account in March but I managed a little in April after receiving the $2,000 CERB – Canadian Emergency Response Benefit..

Number 5 is the one to concentrate on. Build up my emergency fund. Over a 6 month period I had around $2,000 in emergency veterinary bills. I paid on my credit card and then took the money out of my emergency fund to pay the bill when it came in. Due to unemployment I’ve had other priorities over replenishing that money.

Yeah, just paying for my basic needs. No frills girl here!

Who cares about my money?

How do you like the title of this blog post?

Nobody cares more about my money than I do.

I’ve said it before around here.

Now you say it too.

Go on. Say it out loud. Unless you’re reading this at work. Then sssshhhh!

Actually this was kind of sneaky on my part. I decided I want to talk more about an emergency fund but not in a preachy kind of way.

You got me?

I got you.

Let’s tackle this.

Reassessing the emergency fund

Since the coronavirus has changed our lives so dramatically, it’s time to pay attention to the emergency fund.

It’s kind of like a diet. You have a desired weight goal to reach. Once you get there, that doesn’t mean you can start eating as much as you want and putting the weight back on. It means you have to watch what you eat to maintain your desired weight.

Same story with my emergency fund. I have to maintain it. If I keep taking out money for emergencies without replenishing it, one day it’ll all be gone. All my hard work and sacrifices. Gone. Nothing to show for it.

Sob!

My emergency fund is at EQ Bank in a high interest savings account (HISA). EQ Bank has a goal setting tool that I’ve used before, last year for contributing to my TFSA. This year I didn’t set that tool up. Premonition? However, at the end of April I set up the goal tracking tool for my emergency fund. My goal is to bring it back up to where it was a year ago. I’ve given myself until May, 2021 to achieve this goal of saving $2,000 into that account.

I’m thinking that’s an achievable goal. Plus I’ve already thought up a couple ways to help accelerate repaying that $2,000. Will share more on that in another post.

Let’s talk emergency fund

I’ve talked about emergency funds in other posts. Check them out here if you’d like a review.

Being a Single Woman and Dealing with a Bank or Credit Union

Taking Control of Debt on a Low Income

How to Save Money and Bust Debt

Changing your Money Attitudes when you’re Suddenly Single

New Year’s Financial Resolutions Challenges on Low Income

Mostly, I suggest Dave Ramsey’s advice from his book The Total Money Makeover that you can read more about in some of the above posts. Be super-charged intense about saving $1000 into an emergency fund ASAP. Once you have it, then start busting up your debt. Once you’ve got your debt under control, then take that money you used every month to pay down debt and throw it at your emergency fund.

What do you need an emergency fund for?

Well, for something many people are going through right now.

Unexpected job loss.

Your emergency fund will help cover your basic living expenses until you have an income rolling in again.

If you have an emergency fund, this will be your financial safety net for unexpected expenses.

Reasons you need an emergency fund

Besides job loss and no income, here are a few things I’ve come up with why you need an emergency fund. And yes, most of this list – personal experience.

- The car breaks down and needs a new engine

- The car is a write off after an accident and you need to buy another car

- The hot water tank needs to be replaced

- The furnace needs to be replaced

- The roof needs to be replaced

- The fridge needs to be replaced

- Your pet is in medical distress and requires emergency veterinary treatment

- You need major dental work done (and your work doesn’t have a health plan)

- You need to buy prescription medicine

- Other unexpected medical expenses not covered by health care

- The basement floods, thanks to an overflowing river

- An unexpected death in the family

- Divorce

- Lightening hit a tree in your yard that crashed through the living room window

Those are all good reasons to dip into your emergency savings.

What is not an emergency?

There are many things that could leave you short on cash that you might consider an emergency. They’re not what I’d call an emergency where you’d need to dip into your emergency fund. The things I’m listing below, you can start up a separate savings account devoted to these expenses.

Some things I’ve come up with:

- A Hawaiian vacation (or fill in the blank for another destination!)

- Your wedding (and honeymoon)

- Buying a new horse (or other pet)

- Car insurance

- Taxes

- Buying or renovating a house

- Boat

- Motorbike

- Baby

- Clothes

- Jewellery

- Investing in the stock market

- Furniture

- Black Friday sales

You get the point. These items I’ve listed are not urgent or necessary = not an emergency.

It’s the same question you should be asking when you pull out your credit card: is this urgent? Is this an emergency?

Certainly, yes, I’ve had to use my credit card to cover an unexpected bill and then paid back the credit card from my emergency savings account.

Unfortunately, a lot of people have to use their credit cards to cover an emergency, and have no available funds to pay the bill when it arrives.

Building an emergency fund

If you’re in the fortunate group who hasn’t lost their job – yet – you definitely should be thinking about starting an emergency fund. This pandemic is your wake up call. Get moving!

Everyone else, use any available money to cover your basic living expenses. You can worry about putting money into an emergency fund once you’re back at work and your life is starting to regain some normalcy.

Dave Ramsey says to be gazelle intense and get $1,000 into the emergency fund as fast as you can. That means slashing unnecessary purchases. Do you need to stop off for a donut every morning? Do you need to bring home a 6 pack of beer? If you can do without for while, throw that money at your emergency fund.

Ramsey also recommends taking on a side job such as delivering pizza.

As luck would have it, right now there are a lot of openings with restaurants and food delivery apps looking for drivers. Also, Instacart must be short of shoppers/drivers. I’ve received at least two emails from Instacart in the last month encouraging me to apply as a personal shopper.

Set up an Excel spreadsheet or find a free app to track your spending, and figure out where you can cut back from while you’re saving up your emergency fund.

Do you really need cable? Could you go without and disconnect it while building an emergency fund? Watch TV shows on the Internet and movies on YouTube. You can always sign up for cable later on.

What about that landline? If you have a cell phone, do you need both?

Are you eating out?

Do you have a gym membership?

Figure out where you can spend less money, and redirect it to your emergency fund. Even if it’s only $20 at a time, get a fund started. Build up the momentum!

How much money?

Let’s figure out how much money you need in your emergency fund.

Let’s start with that first $1,000.

Once you’re reached $1,000, keep putting money into your emergency savings until it’s doubled. So let’s do that. Double your money at least a couple of times. Your emergency fund might need to hold $5,000 before you can breathe a sigh of relief. But don’t stop there, because you just know something bad is going to happen to your car or your teeth.

Most experts say you need an emergency fund that will cover three to six months of expenses.

Yeah right. For us low income earners all we have to say is “dream on”.

But really, this pandemic is the wake up call. What can you do, at least short term, while you rapidly build an emergency fund. Taking on another job like delivering food isn’t for always. It’s just something you have to do right now until you have an emergency fund that you’re comfortable with that gives you breathing room.

Same if you shut off your cable and redirect that money into an emergency fund. That’s not something you have to do forever. You can hook up the cable once you’re happy with the amount of money sitting in your emergency fund.

Where to stash your emergency fund?

Now, what to do with that emergency fund you’re saving?

Well, you could hide it somewhere in your house if you’re comfortable having cash on hand and have a really good hiding place.

It’s always better to have your money work for you and make you a little bit of money.

Once your emergency fund is over $2,000, you want to keep it in a high interest savings account and that will probably be an online bank. It’s tougher to access those funds, so you’re not going to be tempted to dip in for that new couch you want to buy. Nope. Not an emergency! If you can’t access the funds immediately, that eliminates temptation.

Keep $1,500 or so in your regular bank that you can access quickly if you need to. Or if you’ve paid off your credit card and have a zero balance, that can become your temporary emergency fund.

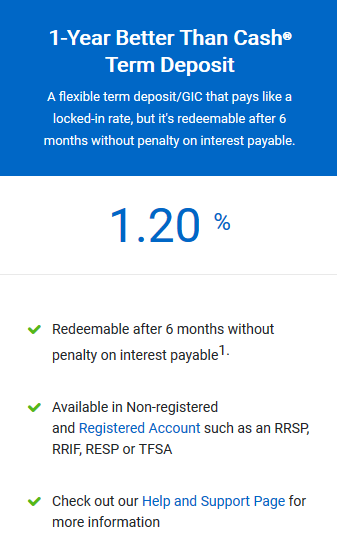

In the past, I’ve kept some of my emergency fund in a term deposit/GIC. I always chose a cashable one, like cashable after 30 days and even one at six months. You don’t want to have your emergency fund locked in for too long. You want to access it quickly in case of an emergency.

Here’s a screenshot of the “better than cash” 1.2% interest one year term deposit, cashable after 6 months, currently offered at Coast Capital Savings.

EQ Bank has an everyday no strings attached savings account with a 2% interest rate. It’s a no-brainer which one’s the better deal. (Edited Oct/20: interest rates in Canada have been dropping and EQ Bank has dropped to 1.5% – still higher than any other bank in the country.)

Tangerine Bank, another online bank, offers high interest rates for new accounts. As of May, 2020, the deal is 2.8% interest for five months and then drops to their regular interest, currently .25%. And yes, that’s a decimal in front of the 25! A quarter percent.

Pssstttt – go with EQ Bank!

Edited to add: EQ Bank has announced a refer a friend program with a $20 bonus for new clients! Yay! If you’re Canadian and thinking about doing online banking with EQ, use my referral link: https://join.eqbank.ca/registration?code=CHERYL1492

Disclosure: I’ll also receive a $20 bonus for each new client I refer.

How did I do?

I hope I didn’t come off as too preachy. I don’t want to sound like one of those financial experts that says well you should have an emergency fund.

Nobody saw Covid-19 coming. Now that it’s here, does that mean people with emergency funds have nothing to worry about?

Even with an emergency fund, I’m still panicked. I might have a few more months breathing room over somebody else who doesn’t have an emergency fund, but if I have to keep dipping in, eventually the well is going to run dry.

While coming up with Nobody Cares More About My Money Than I Do, I hoped to avoid coming across as one of those “if I can do it, so can you” people – which is pretty arrogant. Everyone has different circumstances and different incomes and different emergencies. After I became single I knew I had to scrape an emergency fund together to make my life less stressful. I know what it’s like not to have income, bills piling up, and a deadbeat ex not paying support.

The only person I can count on is me.

I had to figure out a way to make an emergency fund happen. Life changes. Moving to my current rental saved me hundreds of dollars a month that was put toward paying off credit card debt.

For the most part I’ve cut out restaurants and entertainment that cost too much money. The money I save doesn’t necessarily go to an emergency fund, but I have other savings accounts like investments and travel that are hungry for contributions.

By the way, that travel account hasn’t seen any contributions in months. Not a priority.

Life changes. Figuring out priorities. Sometimes you have to write down what’s important and what’s not so much to figure things out. When it’s out of your head and staring back at you on a piece of paper it becomes more real.

Just like the only person I can count on is me.

I know the only person you can count on is you.

Drop me a line if you need any encouragement.

I’ve sure got the time. I can be a good sounding board.

One more thing

I saw this article on Yahoo that just makes you ask what’s wrong with people. A security guard, a father of nine, who works at a dollar store was shot and killed after telling a woman she couldn’t come in unless her daughter wears a face mask. A senseless tragedy brought on by the coronavirus. https://www.yahoo.com/news/security-guard-father-9-shot-224138508.html

Let’s remember the sick, the dying, their loved ones.

I have my health.

What about you?

More reading:

Yeah… it’s really shocking what’s going on right now in the world, but most especially the U.S. Shot over a mask? I was so mad when l read that, just one of the many senseless deaths. This is a great post. An emergency fund is vital. No one needs a new horse…. haha! I think we should be prepared for a whole lot of hurt before things get better.

Thanks Kemkem. It’s shocking to read some of the things going on in the world. Around Vancouver there has recently been an onslaught of hate crimes against Asians. It’s just not acceptable. People are just doing their jobs. They don’t make up the rules. They have to make sure customers are complying with regulations. If you don’t like the rules, just stay away. Why did that woman need to take her little girl shopping anyway? A 9 year old is old enough to stay home alone during daytime hours for a couple of hours. Or her dad could have been watching her. Apparently he had nothing better to do with his time than go around executing over the top vigilante justice.

As for the horse – I need one to help keep me sane! Ha ha. My little guy is having his Sweet 16 in a couple of weeks. I need to get busy on that post!

[…] Can you Handle a $2,000 Emergency? Nobody Cares More About My Money Than I Do […]

[…] this is a refresh of an article I wrote in 2020 where I had a lot of references to Covid-19 because we were living in a pandemic back then. […]